07-05-2013

Oswaldo Lairet – Sequoian Financial Group Research

Summary:

Since our start in 2005, we have sought to keep reports entertaining, even while including the charts, links, mathematical proofs or documentation supporting our opinions. Like our 2006 and 2007 reports, this one is meant to warn you in advance of potential market trouble. This time, however, we set up a hedging structure that may help you protect your current investments from such a possibility.

Foxy Loxy:”How do you know the sky is falling?”

Chicken Little: “Well, if you look at Chart 1, since Dec.11, the total amount in OTC (Over The Counter) Derivatives Notional (Notional), as published by the BIS (Bank for International Settlements) has been hovering near $650 trillion, the level it reached, heading into the Jul.08 market collapse!”.

Foxy Loxy: “Actually, if you had included all contracts in your slightly-outdated chart, the figure would be closer to $700 trillion by Jun.12 and that´s not counting the $300 trillion that were effectively subtracted from pre-2010 aggregates through “Notional Compression” in IRS (Interest Rate Swaps) and CDS (Credit Default Swaps).”

Chicken Little: “Are you saying that, in terms of pre-2010 Notional, the Jun.12, BIS aggregate was really One Quadrillion Dollars (one thousand trillion USD)? That would be almost twice the level of Notional at the start of theHousing Credit Crisis ($586 trillion), marked by Dec.07 in Chart 1″

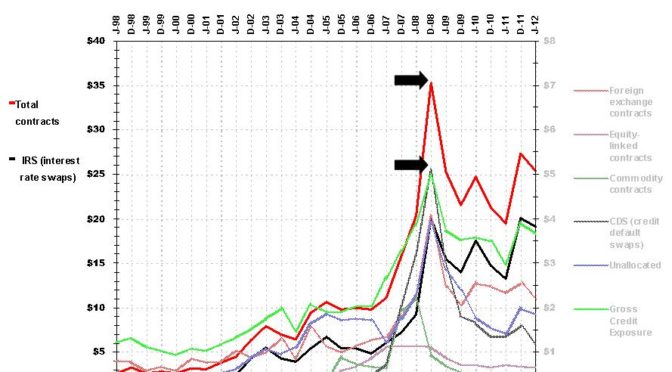

Foxy Loxy: “Yes, but Notional itself doesn’t represent ON or OFF balance-sheet risk, it´s a nominal value upon which derivative-market participants compute a percentage to settle periodically, among themselves. AND …of course, it´s also “the living proof” for every fantastic legend out there, whether it´s planetary hyperinflation, gold´s inevitable rise to $5,000/oz or the “end of (take your pick) …the US dollar” …all fiat currencies” …the financial system” …modern civilization”, etc. What these sources never mention is that next to Notional, the BIS table shows GMV (Gross Market Value) and quite explicitly, the actual balance-sheet risk: GCE (Gross Credit Exposure). In fact, using the same BIS table you used to draw Chart 1, I drew Chart 2. But, note that from Dec.08 to Jun.12, while Notional hits $6 to $7 hundred trillion in Chart 1, GCE actually drops from $5 to $3.7 trillion.”

Chicken Little: “Funny you´d mention that 25% drop in GCE, having just acknowledged that 30% of Notional magically disappeared from the aggregate after 2010! Also, while referring to the $5 trillion top in GCE, you forgot to mention howthe world´s financial system spiraled “like a headless chicken” into that amount! Oh well, I´ll fill you in: When markets were collapsing in 2008 and net settlement obligations had reached $5 trillion, banking giants had only $3.1 trillion in collateral (at market price) plus $1.2 trillion of net worth (tangible equity as opposed to Tier 1 capital). In case you want to keep as a secret “who put up the missing $700 billion” or want the whole episode to remain unreported, as themedia did “not to scare anyone”; just have one of your high-placed, furry friends reap page 20 from this sobering OECD recount.”

Henny Penny: “Sorry to interrupt Chicky pie! But, you forgot telling Foxy dearest, that Notional Compression is a lovely, but rather sumptuous manner of saying “Netting”, which in our last brush with systemic meltdown, didn’t quite work as advertised by those charming young fellows at “Sacs of Gold”! Had the Fed not intervened to save the bottoms of our beloved “netters“, just the CDS blowup at AIG (American International Group) on its own, would have many of them, furry critters from around the planet, still “netting” in bankruptcy court! Again, my apologies and heartfelt thanks for accommodating my disruption.”

Chicken Little: “Much obliged! Henny Bunch! I am glad; all of us birds are keeping track of Foxy´s unintentional slips of memory! I was about to say that if Notional is irrelevant, then: why did rollovers from Dec.07 to Jul.10 in Fed letter-soup, liquidity-programs credits reached over $16 trillion for the banks listed on page 131 of the GAO Report to Congress? And why then, is Reserve Bank Credit (short-term liquidity assistance) still rising in Chart 3, having already jumped 600% since Aug.08?”

Foxy Loxy:”You really are …the ultimate Chicken Little! Why would anyone add up the nominal size of rollovers? Theonly conceivably useful information from that report page is the relative amount of assistance received by each of those banks! Regarding Chart 3´s significance, just answer one question for me: Has any of you birds, experienced anything close to a 600% increase in Real Economy prices since Aug.08? By the same token, take a good look at Chart 4 and note that not even doubling public debt to $16 trillion (in red) since Aug.08, has kept Money Velocity (in green) from falling to a 67-year low! Oh, and BTW, notice how the banks you criticize so much, have actually slashed $3 trillion of their own debt over the same period (in blue).”

Turkey Lurkey: “Foxy dear, you really need to get out of the woods more often! Banks didn’t stop borrowing out of self-restraint! What keeps decimating the aggregate balance of US financial debt is brutal interbank-lending attrition! Remember that following the world´s “Lehman Moment” the TED spread spiked 500% because banks worldwide stopped lending to each other and didn’t budge until central banks intervened? Well, from that point on, interbank lending has continued to implode as much of the maturing bank debt is being repaid by central banks. That´s why Chart 4’s $3 trillion drop in financial debt, coincides with Chart 3’s $3 trillion top in Reserve Bank Credit.”

Foxy Loxy: “Darling, you obviously skipped the chapter on Fisher´s equations in your Econ.101 elective! But, never mind, just Google up “MV=PQ=GDP” and be sure to check what each letter means! If you still don’t get it, here is what´s really happening: Banks have generally trimmed down on interbank borrowing, not only to diminish their dependence on wholesale funding, but also, because they can’t start lending massively to unqualified borrowers a la “pre-housing crisis” style, while qualified borrowers have been repaying debt and decreasing new borrowings. So, while money turnover (lending) decreases and Monetary Base (M) increases, Money Velocity (V), which is the quotient betweenthe two (turnover as dividend and M as divisor), must drop in value! In effect, what´s behind the drop in interbank lending is a drop in Economic Demand, which in turn, affects Output (Q) and Price (P) and thus, GDP.”

Chicken Little: “Wow Foxy, that´s quackery only Ducky Lucky would understand! That is…until Chart 5 confirms to him, that domestic orders (green) and imports (red) are up 26% and 29%, respectively, over their 2009 lows! So, your argument that “demand contraction” is behind the drop in Money Velocity is probably unfounded! Regarding Fisher´s monetary interpretation of Mill’s equation of exchange, you should know that it’s meaningless in the absence of interbank lending. Again, I’ll fill you in: In the centuries after the arrival of central banking, most observers had posited that fractional banking had a measurable effect on M and therefore on GDP. By the time Fisher formalized that relationship, using Mill´s formula, he realized that although you can control M, through central banking, V needs to be an unbound (independent) variable. That is possible, only if “fractional lenders” (private banks) have “unconstrained” access to funding from other fractional lenders (the interbank market).”

Turkey Lurkey: “That might explain why $3 trillion of incremental Fed liquidity plus $8 trillion of incremental public debt have not been enough to outweigh $3 trillion in financial debt reduction. Obviously, public debt has none of the“fractional banking” power of financial debt, but the Fed’s money printing does! If the power of fractional banking is not working for the Fed, could it be, because much of its newly-created liquidity assistance has gone to repay the creditors of undercapitalized banks? If so, then a substantial part of incremental Fed liquidity is not available for bank lending.”

Foxy Loxy: “WHAT? What do you mean?”

Turkey Lurkey: “Well, Foxy, let’s say Bank ABC lost its capital during the credit crisis, as the value of its assets dropped below the sum total of its capital plus liabilities. But, then Lehman happened and regulators decided that, to avoid “financial catastrophe”, banking system losses should go temporarily unrecognized (A la Japan circa 1990). Since ABC’s debt was mostly short-term and from wholesale lenders, it needed to borrow funds quickly against the registered-value of its value-impaired assets. Since only the Fed can create money from thin air, this was the only entity that could lend against ABC’s assets at registered-value. Next, the Fed took ABC’s assets onto its balance sheet and lent itthe funds to repay its creditors in full.”

Ducky Lucky: “It gets even worse Foxy! By lending against the registered value of ABC´s credit portfolio, the Fed not only extinguishes interbank lending (which could still occur at some price below registered value), but eliminates thepossibility of negotiated renewals, which would preserve some of the interbank debt outstanding. Over time, as each new dollar of repayment, unwinds a geometric multiple of credit-dollars created over three decades of unconstrained interbank lending, Money Velocity approaches its historical minimum.”

Foxy Loxy: “So there is no bank hoarding of excess reserves, as much of the 600% increase in short-term liquidity assistance provided by the Fed since 2008, has gone to repay pre-crisis debt on the books of bank-creditors! In theprocess, capital markets have not been allowed to clear prices for pre-crisis financial assets, effectively suspending interbank lending and with it, the astonishing amount of leverage that fractional banking could be providing to theunderlying growth potential of the US economy.”

Chicken Little: “Exactly why THE SKY IS FALLING!”

IN OUR NEXT ISSUE, GOLDILOCKS & THE THREE BEARS DISCUSS, OVER PORRIDGE AND COFFEE:

- Why central bank “assistance” and not inflationary expectations, is the reason behind the post-2008, price-rise in Currencies, Commodities, Stocks and all other types of “Marginable Securities”.

- Why Inflation and Deflation are determined by Central Banks.

- How RWA (Risk Weighted Assets) and other Tier 1 Capital allowances are promoting “London Whales”.

- The launching date for Systemic Risk Averse Fund of Funds (SRAFOF), developed after years of research on which are the key strategic, operational and legal systemic issues to hedge for.

Leave a Reply