February 26, 2023

What the NYFED describes in The Bitcoin–Macro Disconnect as “Bitcoin’s price puzzling disconnect to monetary news” is coincidentally the pattern I came across in December 2022, while methodically tracing all 14 years of the BTC/USD price curve.

Though they don’t express it as clearly, what Messrs. Benigno and Rosa describe in their paper is the same marvel I happened to discover, while helping to write the 2022 annual report for a hedge fund management company I advise:

Since inception, 14 years ago, Bitcoin’s full price-cycle (peak to trough and back) has been patently agnostic to rate policy changes, liquidity events, inflation expectations, and other macroeconomic news.

So, what does this Bitcoin Chart prove?

The degree of disconnect between Bitcoin’s inbred price cyclicality versus the surrounding macroeconomic environment evidenced by Bitcoin’s 14-year price chart above, is positively mind-boggling. Not only for the FED, but for those of us who have spent decades researching financial and economic history. While pursuing a career in Treasury Operations & Trading, the heart of the banking system’s most advanced monetary-intelligence, instant vs historical data analysis, and trading-arbitrage algorithms, I never came across such a wonder.

More Stock-to-Flow, Rainbow Charts, etc., right?

From the start, I found the pattern had nothing to do with the Rainbow Charts or the Stock-to-Flow Model referenced against the Gold supply-demand curve, whose fiat price became easier for the Plunge Protection Team (PPT) to manipulate ever since Volcker began raising policy rates in the early 80s. An incentive arrangement that slowly weakened gold’s allure versus holding fiat and allowed COMEX Gold Futures to begin patently swaying Gold Spot prices.

Since then, the issuance of uncovered gold certificates by the London bullion banking establishment in coordination with G7 central banks has been fully impairing the gold-price discovery process up until the present moment.

So, when the NY FED says:

“Bitcoin shares most of the features of a store of value, such as Gold. But unlike other U.S. asset classes, Bitcoin is not affected by monetary and macroeconomic news.”

What they are not explaining is why Bitcoin is impervious to fiat manipulation. Here is how I answered that question in December, after weeks spent reconfirming the price data, crunching empirical proofs and researching all related scientific fields, until finding the biological, cultural, and economic tenets that support the thesis laid out below.

INTRINSIC VALUE derives from nothing else, but the preservation instincts that are deeply rooted in scarcity vs hoarding behavior in humans. Some of these instincts are survival traits inherited from biological evolution, others come from cultural resource competition dynamics thoroughly detailed in the post below.

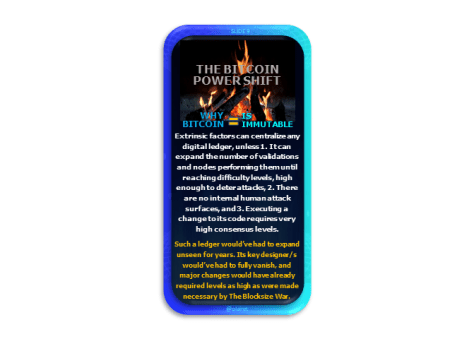

Which suggests that it’s infinitely easier to game our primal instincts, than we’ve been taught, and that whoever designed the Bitcoin algorithm is acutely aware of how these preservation instincts work in humans at a collective level. Thus, while PoW‘s validation procedures make Bitcoin’s unhackable by anyone, including insiders (footnote), Halvings impose the self-reliant monetary policy (see code below) that triggers the self-preserving mechanism described above.

Bitcoin’s Game Theoretical Dynamics

Activating human preservation instincts in a group, regardless of its size, that fully understands the mathematical principles sustaining Bitcoin’s immutability seems to sufficiently determine its fiat-price progression path, once it starts.

Conversely, no matter how many speculators, “crypto” schemers, and otherwise uninformed fad-seekers come and go, their participation, or lack thereof, seems to have no persistent effect over time.

In sum, Bitcoin’s long term price path seems to depend only on the collective response of a small group of investors who hold a relatively large proportion of its total issuance. A group whose high degree of technological, financial or mathematical knowledge allows it to stay fully invested, regardless of Bitcoin’s large fiat-price oscillations, or its constant exposure to political, uneducated, falsified or intentionally orchestrated mediatic attacks meant to misinform the general public and distort the average investor’s price-discovery process.

The Proof of The Pudding has a Conclusive Taste

If you split Bitcoin’s 14-year price chart into 4 lines each for the halvings (blue) & their midpoints (grey), you find that each peak to trough cycle has pivoted up or down over the same time interval between each color pair.

To visualize these dynamics I drew blue verticals for each halving date and grey ones for each midpoint date. As the chart shows, Up Legs start about two years before halvings and end about one year after them, lasting about 1000 days. That is when Down Legs start: a few months before midpoints and they end a few months after them, lasting about 400 days, Which drove me to conclude that by:

Note also that Up Legs until now, seem confined to return no higher than ~20% over the immediately previous high return, within their ~1000-day period. This has occurred persistently between the months before and after each halving. While Down Legs seem confined to a return loss no higher than 80% of the immediately previous high return, within their ~400-day period. This has also occurred persistently between the months before and after each Midpoint.

Finally, here’s why we can’t just pick and choose the last +400 Day bottom. Until the “Latest Bottom” hypothesis is proven (at the end of the present cycle), we cannot firmly establish its precise date or price. All we can do is theorize its value ex-ante (via interpolating the last two ex-post time period samples -as shown in the excel sheet below).

In short, December 26th is not even the December price low, it results from averaging the total amount of days that elapsed as the last two ex-post lows were reached. The same goes for the price and date at the end of the dashed white lines, on the top chart. Those ex-ante y and x values are merely projections trained on the confirmed ex-post values locked on top of the partial ellipsis formed by the slope of the secants dropping off.

* BTC’s PoW turns energy into a generic entry fee to preserve miner & block-winner anonymity+unpredictability & BTC’s immunity; while turning their ASICS & all other participating nodes into a global server that can’t be rigged, monopolized or altered to hinder Bitcoin’s consensus protocol.

You must be logged in to post a comment.